The OECD global minimum tax: impact on family offices

Sunday 3 September 2023

Gregory Price

Macfarlanes, London

gregory.price@macfarlanes.com

Bezhan Salehy

Macfarlanes, London

bezhan.salehy@macfarlanes.com

The OECD global minimum tax: impact on family offices

For the past two years the tax policy agenda for large international businesses has been dominated by the Organisation for Economic Co-operation and Development’s (OECD) proposals for a global minimum corporate tax rate – known as ‘Pillar Two’ or ‘the GloBE Rules’. Broadly, the GloBE Rules aim to ensure that large groups pay an effective tax rate (ETR) of at least 15 per cent on their profits on a country-by-country basis. Where a group has low-taxed profits in one or more countries, the rules allow other countries to charge top-up taxes to ensure the 15 per cent minimum rate is met.

Countries are currently in the process of implementing the GloBE Rules in their domestic legislation with the earliest adopters – including the UK and the EU Member States – committed to bringing the rules into effect from 1 January 2024.

The GloBE Rules will apply to ‘MNE Groups’ with annual revenues that exceed €750m. In this context, an MNE Group can be any structure that includes entities located in more than one jurisdiction.

While the GloBE Rules are primarily aimed at large trading groups, family offices can’t ignore them. The Rules’ scoping criteria do not distinguish between entities based on their purpose or the type of activity they carry on. Family trusts and investment companies may also therefore be affected by the rules if they meet the revenue threshold and have a presence in a low tax jurisdiction.

When is a family office an ‘MNE Group’?

The GloBE Rules define a Group as the collection of entities that are included in the consolidated financial statements (CFS) of an ultimate parent entity (UPE).

At first glance this definition might appear to exclude many family offices. That is because parent entities in such structures are often not required to prepare financial statements, either because they are located in jurisdictions where that is not a company law requirement, or because they are of a form that is not subject to company law at all (eg, trusts and partnerships).

However, the Rules still apply in these situations. Because the parent entity does not have CFS, the Rules instead use as their starting point the hypothetical financial statements that the parent entity would have prepared had it been required to by law. This means that entities such as trusts, which probably do not consider themselves as group parents, could nonetheless be regarded as UPEs for GloBE purposes.

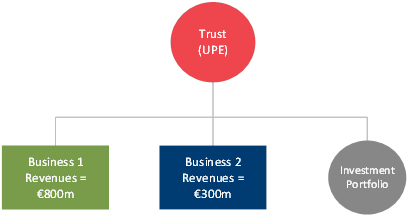

Consider Figure 1, which depicts a family trust that owns two independently operated trading business and an investment portfolio.

Figure 1: Family trust example

Although the trust may not prepare financial statements, if it was required to do so it is likely that it would consolidate all the other entities. For GloBE purposes the trust is therefore the UPE of a single MNE Group. That has the effect of bringing both Business 2 (which, looked at in isolation, has revenues below the €750m threshold) and the investment portfolio into scope of the Rules and potentially subjecting them to top-up tax.

Accounting standards contain some exceptions from the general requirement for a parent entity to consolidate its subsidiaries. The most significant such exception under the International Financial Reporting Standards (IFRS) is where the parent is an investment entity that accounts for its subsidiaries on a fair value basis. Whether a family office can avail of such an exception will depend on the detailed application of the relevant accounting standards to a structure’s particular facts. Where it seems plausible that this will determine whether a family office might go on to meet the revenue threshold (see below) we recommend that directors or trustees take appropriate advice.

How does the revenue threshold apply to family offices?

A group will only be in scope of the GloBE Rules for a given year if the revenues reported in its CFS exceed €750m in at least two of the four previous years.

‘Revenues’ most obviously includes amounts reported as such on the top line of a trading group’s income statement (typically gross amounts received for sales of goods or services). However, the GloBE Rules and accompanying OECD commentary are unclear as to whether economic inflows recognised elsewhere in a group’s income statement should also be included.

For example, many family offices own an investment portfolio alongside a trading business. The OECD materials do not explain whether, in such situations, investment income and gains should be regarded as revenues. Nor do they explain how revenues should be defined for wholly investment businesses – it is unclear whether revenues should include investment fair value movements, or amounts accounted for in reserves.

While in many cases including or excluding these amounts will not make a difference to whether the revenue threshold is met, this is a source of considerable uncertainty in marginal cases.

We understand that the OECD may address this question in future Administrative Guidance that it is expected to publish from time-to-time. For now, though, we consider that directors or trustees of entities facing this uncertainty should take a prudent approach and take steps to assess the potential impact of being caught by the Rules.

What are the consequences of being in scope?

Structures that meet the revenue threshold and are in scope of the GloBE Rules will potentially have to pay top-up tax charges if they realise income or gains that are currently taxed below 15 per cent.

If a group’s UPE is in an implementing jurisdiction, that top-up tax will all be paid by the UPE. If the UPE is not in an implementing jurisdiction, the right to collect top-up tax is shared out among the various entities in the group.

It is common for family offices to hold portfolio investments in offshore financial centres with low tax rates, so investment income and gains are likely to be a key source of potential exposure for in-scope taxpayers. Even if a structure is subject to the rules, however, in practice investment returns may escape top-up tax depending on how they are accounted for, whether they qualify for specific exemptions in the GloBE Rules and whether they are sheltered by other, highly taxed profits.

In-scope groups can proactively manage their exposure by reviewing their accounting policies, factoring GloBE treatment into their investment strategies and considering restructuring.

Conclusion

Family offices are not the intended target of the OECD global minimum tax initiative, but they may suffer collateral damage. We recommend family office directors and trustees review whether there is a risk that their organisation may fall in scope, and if so assess the consequences – and consider options for mitigation.